How did a federal government employee starting with a $30K net worth achieve a $1 million net worth before 40?

16 years of monthly details

Net Worth Stories:

Every Wednesday, we focus on a net worth “story” to help you peek inside someone’s personal finances and get the inside view that nobody usually talks about. This week we have a 40 year old that is married with 2 kids. He is an engineer working for the federal government. He married his wife in 2015 and she now works as a nurse. They currently earn between $150-199K/year.

His net worth history starts in June 2008 (age 24) at $30,585. At this point, he is single and one year out of college. He graduated in June 2007 and is living at home. He has some cash savings and started investing in his retirement TSP (Thrift Savings Plan) at work (similar to a 401(k) for federal government employees). As we’ve been mentioning the last several weeks, saving your first $100K in net worth is the hardest. Why? You don’t really get any of the benefits of compounding that will come over time. You literally have to start saving and investing a portion of your income (forgoing some consumption). You can see below he achieved his first $100K in net worth in October 2010 at 26 years old.

Crossed $100K net worth - October 2010 - age 26

Crossed $200K net worth - September 2012 - age 28

Crossed $300K net worth - June 2014 - age 30

Crossed $500K net worth - January 2018 - age 34

Crossed $1 million net worth - June 2023 - age 39

How did he do this? 16 years of net worth history and details below.

Current Net Worth Composition ($1.11 million):

Retirement (TSP) (51% of net worth)

Roth IRAs (17% of net worth)

Home Equity (16% of net worth)

Taxable Brokerage (6% of net worth)

Cash (8% of net worth)

Car (2% of net worth)

Discussion on net worth composition:

Their net worth composition is heavily weighted toward investments in their retirement account (TSP), Roth IRAs (his and his wife’s) and stocks/bonds in a brokerage account. Retirement accounts, Roth IRAs and brokerage accounts collectively represent almost 75% of their net worth. Home equity is about 16% of their net worth. They also have $81,683 in cash which represents ~8% of net worth. Below includes 16+ years of details in each of these categories to show the steps and actions that together allowed them to reach >$1 million+ net worth before turning 40.

Retirement Savings:

He started saving consistently in his employer TSP (Thrift saving plan - similar to a 401k for federal government employees) with his first job and now his retirement savings make up over 50% of their net worth. Fortunately, he started saving in 2008/2009 during the financial crisis when everything was 30-40% off the previous highs. Even after that, his retirement did experience quite a bit of market volatility. If you zoom in, you can see a ~$60,000 (18%) decrease from February-April 2020 at the beginning of the pandemic. In addition, another ~$108,000 (18%) decrease from January-October 2022. Despite the volatility, they kept investing with every paycheck and now at the end of 2023, they are again at an all-time high of $571,710 in retirement savings. As you can see the first $100K took over 5 years and the last $100K of savings took <1 year due to increasing salary, increasing contributions/match as well as market returns increasing due to compounding over time.

Retirement balances:

crossed $100,000 - February 2013 - age 29 (~5.5 years for first $100K)

crossed $200,000 - January 2017 - age 32 (~4 years for second $100K)

crossed $300,000 - July 2019 - age 35 (~2.5 years for third $100K)

crossed $400,000 - December 2020 - age 36 (~1.5 years for fourth $100K)

crossed $500,000 - August 2021 - age 37 (~8 months for fifth $100K)

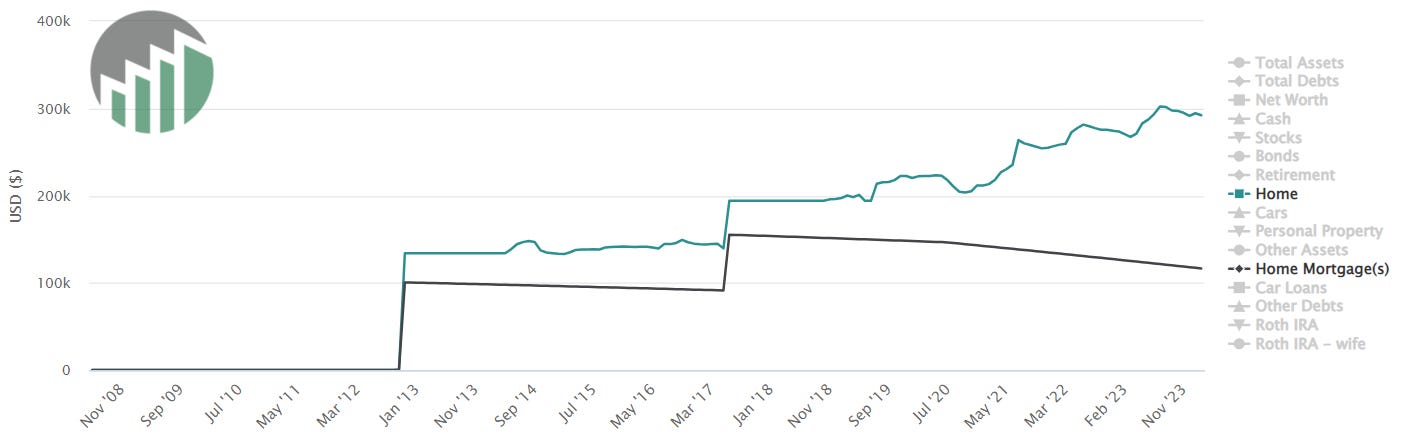

Home (16% of net worth):

Before getting married, he had purchased a $134,000 2 bedroom (+loft) house in Dayton, OH in October 2012 (with a $100K mortgage) while in his late 20s.

They purchased their current home in June 2017 for $194,000 (w/ $155K mortgage) at age 33.

They are currently living in this same house. The mortgage balance is now only $116K (principal paydown of ~$39K since 2017 purchase). In addition, their home value has increased ~50% from $194K to $292K from 2017 to 2024. Total home equity is now $175,750 or 16% of net worth.

Example home commentary on refinancing from a 4% 30 year mortgage to a 2.75% 15 year mortgage in May 2020 (during the pandemic):

Brokerage account / Roth IRAs (23% of net worth)

In addition to investing in his retirement account, they are also saving in a taxable brokerage account and Roth IRAs. One Roth IRA was started in 2010 and the second Roth IRA was started in 2016. The first investments in the taxable brokerage were made in 2013. Combined these accounts are ~23% of their net worth.

Roth IRA (his): $134,069 (started in 2010)

Roth IRA (wife’s): $54,985 (started in 2016)

Taxable brokerage (Stocks/Bonds): $70,009 (started in 2013)

Car (2% of net worth)

After graduating, he purchased a used car with a car loan. In 2008, that car was valued at $12,000 and the remaining loan balance was $8,339. As you can see from the chart below, they have not spent much on cars relative to their net worth. Since they have been married, they have not taken out any car loans and prefer to drive used cars which has allowed them to increase their savings rate. As of February 2024, cars make up only 2% of their net worth.

Example car commentary from March 2019 - they sold a car with 200,000 miles and purchased a used Camry with 90,000 miles:

Comparison to net worth averages/median for similar age

Below we show the median and various percentiles of net worth for someone between the ages of 40-44 and 45-49. This couple is in their early forties with a net worth of $1,114,298 and are just about at the 90% percentile for their age.

Also, the majority (82%) of their net worth is not visible as it consists of financial assets in bank, brokerage and retirement accounts. Another common metric for those trying to build wealth is how much they have in retirement savings compared to their home equity. They have greater than 3X the amount in retirement savings ($571K) compared to home equity ($176K) which is above the 2X average.

This is another great example of following the 5 proven ways to build wealth. 1) focus on gaining skills to increase your earnings 2) start and increase your savings rate as your income increases 3) don’t just save - you need to invest 4) be intentional about spending and 5) minimize debt and lifestyle upgrades (keep driving that same car even with 100K+ miles).

If you’re not already, start tracking your net worth!

If you would like to see more financial information on the individual discussed today, you can click here username: mdv1984 and also follow their path to financial independence. You can also join thousands who are tracking their net worth on networthshare.com and be encouraged monthly by a likeminded community. Also, subscribe to this weekly Net Worth Stories newsletter for real life examples (net worth stories like this and other useful tips to create the life you want!)

NetworthShare helps you calculate net worth, and track it online. You can publicize your net worth anonymously, compare it to others & see where you stack up. You don’t provide any specific account or log-in information like some sites. There are interactive charts that let you slice & dice community data (like those included in this article).

It's also a community of financially like-minded people where you can ask questions, get advice, and share financial stories. You are able to search by your occupation, age range, education level, or salary range and see where you rank!

Looking for more TenWilsons content?

We will also be providing new personal financial metrics that you won’t see elsewhere (examples: net worth composition analysis: % of net worth in home equity vs retirement accounts at various ages; the 8 levels of financial independence; visible vs non-visible wealth). We also recently started doing data visualizations to help turn data into interesting charts and interactive stories. Follow TenWilsons on twitter where you can get daily content and other helpful financial tips.

Feedback or comments?

We want your feedback! Please provide feedback/comments on what information or segments you like most and what you would like to see more of. Thanks!