He followed these 4 steps (in his 20s, 30s, and 40s), became a multi-millionaire, and retired at age 51.

21 years to reach the first million, 4 years to reach the second million, 3 years to reach the third million and 1.5 years to reach the fourth million!

Net Worth Stories:

Every Wednesday, we focus on a net worth “story” to help you peek inside someone’s personal finances and get the inside view that nobody usually talks about. This week we have a 54 year old. He is married and retired at 51 when his net worth reached $3 million. We share the 4 steps he followed to become a multi-millionaire. He also share his best financial decision at the end of today’s article. We hope you find this story inspirational. If you’re in your 20s, 30s, or 40s, there might be one takeaway for you to consider on your path to financial independence.

Below is a graph of his monthly net worth over the last 17 years. What you will see is the power of compounding and saving early.

May 2013 - first million - 21 years - age 44

May 2017 - second million - 4 years - age 48

**RETIRED EARLY 2020 BEFORE PANDEMIC**

Aug 2020 - third million - 3+ years - age 51

Dec 2021 - fourth million - 1+ years - age 52

Feb 2024 (today) - $4.3 million - age 54

Here are the 4 steps that he followed that propelled his savings and net worth over the years. We’ll go into more detail on each of these below:

Started saving for retirement early

Didn’t sell during market downturns

Bought a less expensive home

Minimized interest expense

#1 - Save for retirement early

Start saving 10%+ in your retirement accounts in your 20s and increase % and $ saved as your income increases (avoid too much lifestyle inflation). If you do this, retirement savings should be the largest % of your net worth. Below you can see, he averaged ~55-60% of his net worth over the last 20 years in his retirement savings (401K/Roth IRAs).

age - retirement savings as % of net worth

age 36 - 57% of net worth

age 43 - 60% of net worth

age 48 - 54% of net worth

age 51 - 58% of net worth

age 52 - 61% of net worth

age 53 - 59% of net worth

age 54 - 61% of net worth

#2 - Don’t sell during market downturns

Also, keep invested during downturns. During the last 17 years, there were three significant market corrections (>15% drops). He stayed invested as well as continued with regular paycheck contributions during these down periods.

May08-Dec08 - 42% drop in retirement balances $356,432 to $204,837

Jan20-Mar20 - 18% drop in retirement balances $1.65M to $1.35M

Nov21-Sept22 - 20% drop in retirement balances $2.45M to $1.95M

#3 - Buy a less expensive home

Buy a home that's less than what the bank says you can afford and stay in that same home for 10+ years (avoid buying a new home as your income increases). His equity in his home averaged 18% of his net worth (meaning he had at least 3X as much invested in retirement accounts). This is the difference between visible wealth (house you live in) and invisible wealth (investments/retirement savings).

He purchased a home in 2006 for $350,000 with a $220,000 ($130,000 of equity or ~23% of net worth). As you can see, he staying living in this same home for 10+ years even as his net worth increased past $1M and $2M. His house appreciated to ~$570,000 by 2018 when he sold it. At that time (12 years later), his remaining mortgage balance was $130,489 meaning he had ~$440,000 in home equity which was approximately 18% of his net worth at the time. In retirement, he recently purchased a home for $675,000 (~18% of net worth) and sold investments to pay for it (no mortgage).

By not upgrading his home for 10+ years as his income increased, he was able to increase his contributions to his retirement and taxable brokerage accounts. During this same time period 2006-2018, retirement balances increased from $561K to $1.3M. Also, by starting to contribute to taxable brokerage accounts, he accumulated savings that could be withdrawn in early retirement prior to age 59.5 for retirement accounts.

#3 minimize interest expense

Avoid or paydown all consumer debt and paydown mortgage debt, use money saved in interest expense to increase retirement contributions and start saving in taxable brokerage. As you can see in this graph, he did not have any consumer debt and worked to paydown his mortgage from 2006-2018.

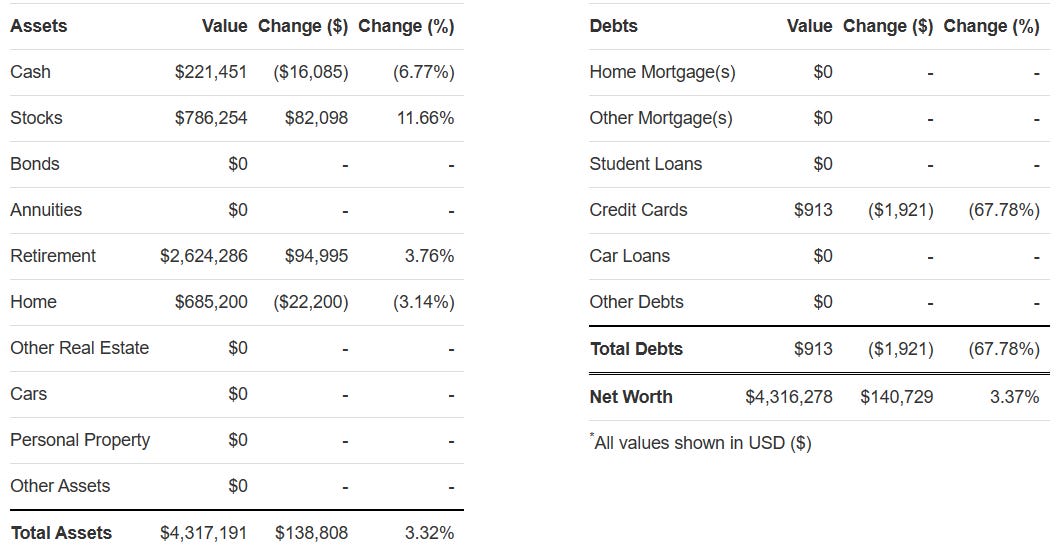

Current Net Worth Composition ($4.3 million):

Retirement Accounts (61% of net worth)

Home Equity (16% of net worth)

Taxable Brokerage (18% of net worth) ← critical to retire early

Cash (5% of net worth)

Comparison to net worth averages/median for similar age

Below we show the median and various percentiles of net worth for someone between the ages of 50-59. This week’s net worth story is a 54 year old with a net worth of $4,316,278. This is 94th percentile at age 54. If he was 55 (and therefore in the 55-59 age range), he would be in the 92nd percentile.

Also, the majority (84%) of his net worth is not visible as it consists of financial assets in bank, brokerage and retirement accounts. Another common metric for those trying to build wealth is how much they have in retirement savings compared to their home equity. He has more than 3.8X the amount in retirement savings ($2.6M) compared to home equity ($685K) which is above the 2X average.

Summary

What does he say is his Best Financial Decision? LBYM

LBYM is living below your means. It is a simple concept: spend less than you earn. Your net worth (wealth) only increases from your earnings that are not spent. Also, as mentioned above, buy and hold during market downturns. Resist the urge to time the market and instead measure time invested in the market. Anything is possible when you give it 10-20-30 years (even early retirement!).

Enjoy your week and see you on Saturday for the weekly summary!

If you’re not already, start tracking your net worth!

If you would like to see more financial information on the individual discussed today, you can click here username: 4eaxfm and also follow their financial path during early retirement. You can also join thousands who are tracking their net worth on networthshare.com and be encouraged monthly by a likeminded community. Also, subscribe to this weekly Net Worth Stories newsletter for real life examples (net worth stories like this and other useful tips to create the life you want!)

Looking for more TenWilsons content?

We will continue to provide new personal financial metrics that you won’t see elsewhere (example: net worth composition analysis: % of net worth in home equity vs retirement accounts at various ages; the 8 levels of financial independence; data of visible vs non-visible wealth). We also recently started doing data visualizations to help turn data into interesting charts and interactive stories. Follow TenWilsons on twitter where you can get daily content and other helpful financial tips.

Feedback or comments?

If you enjoyed this article, please press the like button (at the top or bottom)! Also, what do you think of his 4 steps to early retirement (age 51) or his best financial decision (LBYM). Leave your thoughts in the comments below. Thanks!

In case you missed it! Here is last week’s Saturday Summary with 15 net worth updates:

This is a great analysis and write up. Thank you! I have a question about #4 where it mentions using additional savings where possible to start investing more in taxable brokerage accounts when retirement contributions are maxed out or where you want them to be. This seems to be where I’m at now, but I struggle to think about starting to dollar cost average into the market right now (say on a monthly basis) when we're right in it after yet another record setting bull run. I don't want to try to time the market but it's hard to face the fear this will just be regretted in a few years time at the next correction. Open to any suggestions about how to more optimistically view this, since I think it's a smart next move-- just has me worried about emotions when it inevitably dips.

The key lessons of how to get reasonably rich in America are captured here: Just start saving early, live below your means, minimize debt, keep plugging away (even through the market downturns) and eventually you will be in a good position. Almost anyone can do this if they have the discipline. I like how you broke down his progress visually; as well as showing how much quicker each million came. Great analysis!