"I’m always afraid of getting fired, even when everything goes perfectly at work"

Living in Fear: The Prospect of Job Loss Fuels Financial Security in Oregon

Exploring the Hidden Aspects of Wealth

Welcome to our latest newsletter, where we dive into the financial journeys of individuals across different age groups and life stages. From those in their 20s/30s just starting to build their net worth, to individuals in their 40s realizing the power of consistent saving and strategic diversification, and finally to a couple in their late 50s who transformed their financial situation from a negative net worth to a $2 million net worth.

These stories highlight the importance of financial planning, disciplined saving, and the power of compounding over time. Read on to be inspired, informed, and perhaps find one take-away that you can apply to your own financial journey.

Consider taking one action today to create the life you want tomorrow!

In their 30s:

$218,399 net worth - A 39 year-old front office manager in Portland, Oregon earning $98K/year. She has an accumulated net worth that is 61st percentile for her age group. Her net worth composition consists of $94K or 43% in retirement accounts, $80K or 34% in home equity, and $42K or 19% in taxable brokerage. She discusses (in a financial diary) her financial history, including her parents' thriftiness and her struggle with student loan debts. She has a heightened sense of financial responsibility, often worrying about losing her job and prioritizing savings. "I’m always afraid of getting fired, even when everything goes perfectly at work, so it’s turned me into a little bit of a hoarder with my money. I am trying to focus on the enjoyable objectives, like saving for a good retirement, but I also want the financial security to insulate me from harm if I do lose my job, so having a year or two of income on hand is one of my more immediate (unnecessary) goals."

TAKE-AWAY: The importance of financial education. Although her parents were financially secure, their restrictive approach to money led to issues with spending and saving in adulthood. Parents should look to teach their children about money management in a balanced way.

$672,600 net worth - A 33 year-old program manager in manufacturing in Alabama earning $179K/year (husband earns $142K/year). They have an accumulated net worth that is 92nd percentile for their age group. The largest portion of their net worth $352K or 53% is in retirement accounts (401k), $188K or 27% is in home equity, 14% in taxable brokerage and 6% in cash. They have separate bank accounts, investment accounts, mortgages, and car loans, but they strategize and track their finances together. “My husband and I often talk about strategies to increase our net worth and create generational wealth.”

TAKE-AWAY: The importance of open and regular discussions about financial planning and wealth generation between partners. This emphasizes the need for strategic and collaborative decision-making to achieve long-term financial goals.

In their 40s:

$1,170,000 net worth - A 47-year-old high school teacher and his 44-year-old wife, currently a PhD student, live in Amarillo, Texas. They have an accumulated net worth that is 84th percentile for their age group. Despite never earning more than $135k in combined salary in any year, they have managed to save between 30-40% of their income for most of their marriage. Long-form interview includes topics of career progression, savings strategies, spending habits, work-life balance and investment philosophy. The largest portion of their net worth $438K or 37% is in rental properties, $345K or 29% is in retirement accounts, $220K or 19% is in home equity, $140K or 12% in cash accounts. "It matters little how much you make, all that matters is how much can you save."

TAKE-AWAY: The importance of consistent saving over a long period of time. This also highlights the power of disciplined saving and living within your means, irrespective of your income level as well as the power of compounding.

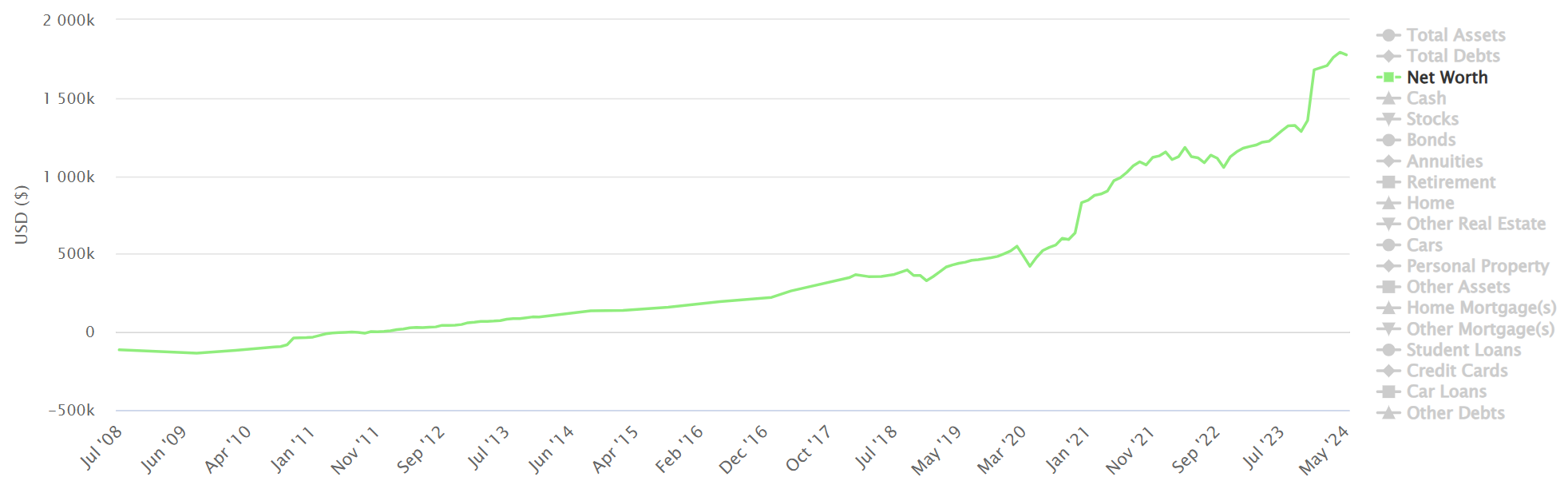

$1,775,054 net worth - An early 40s lawyer living in the midwest earning low $200s annually. Sixteen years of monthly details on NetworthShare.com starting at a negative ($115,000) net worth in 2008. He has an accumulated net worth that is 94th percentile for his age group. The majority of his net worth ~$1.34 million or 75% is in retirement accounts/ pension/ HSA, $255K or 14% is in home equity, and $65K or 4% is in a taxable brokerage.

TAKE-AWAY: Consistent saving and investing over a long period of time can lead to substantial growth in net worth (see graph below that demonstrates this financial journey from a negative net worth to the 94th percentile for his age group.)

$2,100,000 net worth - A married 49 year-old with 3 kids is currently earning $170K and plans to retire early at 55. He has an accumulated net worth that is 92nd percentile for his age group. His net worth composition consists of $825K or 39% in retirement accounts (401k, Roth 401k and HSA), $600K or 28% in home equity, $390K or 19% in taxable brokerage, and $260K or 12% in cash (CDs, HYSA, Checking). They anticipate their net worth to be $2.5 million dollars or more by the time they retire (age 55). They have three children, two of whom they anticipate will be in college when they retire, and one who will be in high school. They estimate their monthly expenses to be between $5,000 to $6,000 dollars, including travel. "I know if you are employed and contributing to 401K, you can quit and start taking distribution at 55 without any penalty."

TAKE-AWAY: The importance of diversified investments and savings strategies to achieving financial independence and/or early retirement (FI/RE). He has contributed to a variety of pre-tax and post-tax accounts that create a way to fund the gap from 55 to 59.5/62 if he decides to retire early.

$5,300,000 net worth - A couple (both aged 43) with 2 kids, reported a significant increase in net worth, largely due to their compensation. See 3 previous updates on net worth (1 year ago, 2 years ago, 6.5 years ago). Their 2023 Adjusted Gross Income was $2.1M, and they paid approximately $1M in federal and state taxes. They have an accumulated net worth that is 98th percentile for their age group. Their net worth composition consists of $1.9M or 36% in taxable brokerage accounts, $1.6M or 30% in retirement accounts, $1.2M or 22% in home equity, and $500K or 9.4% in cash. “Corrected my poor investment choices of prior years by shifting >80% into VTO-like ETFs.”

TAKE-AWAY: The importance of keeping investment selection simple and cost-effective. The author corrected past mistakes by shifting over 80% of their portfolio into S&P500 Index ETFs, which are generally low-cost and diversified. This strategy not only simplified their investment approach, helped increase their net worth, and demonstrates the value of a straightforward, affordable investment strategy.

In their 50s/60s:

$1,989,542 net worth - Adrien and Rob, ages 59 and 62 respectively, openly discuss their financial journey on a 2 part podcast (part 1, part 2), from being in deep debt to accumulating a net worth of $2 million. They have an accumulated net worth that is 83rd percentile for their age group. They candidly share their money fears, especially Rob who admits to living with a lifelong fear of money. Rob's fear becomes more apparent in their discussions about their financial future, and he worries about their ability to sustain their lifestyle in retirement. "I would say I've been worried about money for about 57 years as soon as I became old enough I really thought that our family was going to run out of money for food."

TAKE-AWAY: The importance of financial security from a young age and the long-term impact that financial worries can have on an individual's perspective on money for their entire life.

What is the meaning behind Ten Wilsons?

The $100,000 bill is the highest denomination ever issued by the U.S. Federal Government. Woodrow Wilson is the president on the $100,000 bill.

Looking for more TenWilsons content?

Follow TenWilsons on twitter where you can get daily content and other helpful financial tips.

If you’re not already, start tracking your net worth!

Join thousands who are tracking their net worth on networthshare.com and be encouraged monthly by a like-minded community.

Please like and share with others!

If you enjoyed this article, please press the like button (at the top or bottom) and consider sharing it with others!

6 net worth updates from this past Wednesday!

11 net worth updates from last weekend!